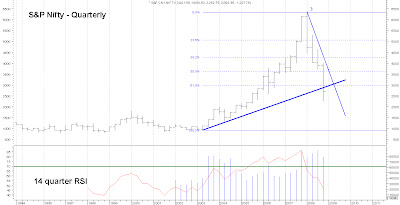

From September onwards every worthwhile technical level was broken with impunity and even long term supports as shown were given no regard what –so- ever. Major retracement supports have also been broken. This to me essentially means that the underlying forces that made this pattern is undergoing a structural shift and that a new set of forces are emerging which are going to determine the pattern in future. How this will shape can be speculated only when these new forces start manifesting itself in a clearer way.

From a fundamental perspective it means that the current meltdown is just not business cycle induced but there is probably a new landscape developing wherein future business will be conducted. This arises from the fact that the excesses on the upside were caused by risk taking levels that were unprecedented and as the risk is unwound the implications to the financial and real economy are much severe and greater than a normal business cycle related downturn will cause. This then calls for huge intervention by government and when it happens in a global scale where everyone is gasping for breath, there are no saviors. Everybody while trying to hold each others hand is also wary that the other person does not try to capitalize on the situation and weaken him.

These are once in a century kind of events. To understand this better let’s take the period post the great depression. When things started looking up finally, having been bruised badly, the conservative mindset was dominant. So at any slight sign of excess players would unwind and reduce the risk quickly. This helped in more sustainable move up with much lesser volatility and uncertainty. But as years passed and a new set of players came – those who had not seen or felt the pains of the past and were witness only to the better times had a different risk profile and were willing to take greater risks. However they had the advantage of hearing firsthand about the depression and its related consequences. So, while the scale of movement on the up and down increased, their minds were also tempered by what they had heard and read much more than would the next set of generations. With time as new generation of players came who were much more distanced from the past pains and their risk appetites kept increasing. It cumulated over time to reach a level that now can be considered as the tilting point. So here we are. We would now see a number of changes that in the opinion of the wise in the governments and the intellectuals they call upon, is a safer environment to conduct business. I have elaborated this theme in my previous posts and ‘am not elaborating it any further.

So where does India stand in this? India has integrated with world economy in the past five years so much more rapidly than it did the decade prior to it. The kind of move that the Indian stock market made on the up was due to cheap money that came from sources outside India. Hence any major shifts in the environment in those markets which originated this cheap money are going to impact the Indian markets as severely. However well Indian companies do there will be no bull market without money flow in volumes.

Let’s look at some of the fundamental pointers which tell us that India shall be shaping up in close correlation to how the new world economic order evolves. Keep in mind that India’s external trade already constitutes over 40% of its GDP. Net investments by FIIs (Foreign Institutional Investors) in Indian stock exchanges by January 2008 were USD65 billion. In the last four years India has received USD50 billion as FDI (Foreign Direct Investment).

1. Rupee has depreciated against dollar to its lowest ever in its history (more than INR50 to a USD – a 27% depreciation YTD). This is lower than in 1991-92 when India pledged gold with Bank of England for getting a foreign currency line to fund its imports – which to me is the low this country saw in its financial history.

2. The kind of action that RBI and finance ministry has taken to ease liquidity and interest rate in the past four weeks is unprecedented. About INR2trn. (USD40bn.) was released into the system in a period of 3 weeks. The RBI has even gone ahead and approved lower risk weight age and changed the delinquency or NPA recognition standards for sectors such as real estate and infrastructure thus aiding bank balance sheet manipulation. This shows desperation and one has to read in between to understand where we stand. Despite such huge moves the money flow is still stagnant and the markets are only seeing downward pressure. It would probably have worked if the issues were India specific which is not the case.

3. The corporate leverage is the highest ever. When you listen to bank chairman saying companies do not want to take further leverage on their books and are not drawing down funds you it becomes clear that the company’s major business risks ahead therefore do not want a double whammy of financial risk also to take them down.

4. And where the companies are willing to take debt banks seem to become risk averse and are not lending. Most small and medium enterprises, which comprise of more than 40% of production output, are a victim. Banks also fear a fairly large write-off in this segment and hence do not good money to become bad.

5. The real estate sector which was the leader in the last up move is in dire straits. Some of the highly leveraged high profile companies have put many of the large projects on the block as debt repayments are due in the next six months to one year and there is little hope of rollover. Most real estate companies did not participate in Friday’s up move reflecting this. This sector will have to change its business model and the land bank game is a goner. Don’t expect to see any major up move in land prices for some time as many of them move to the auction block.

6. Infrastructure companies also had leveraged themselves highly as the government moved to the BOOT and BOT models. Now with scarcity of capital and high cost most projects will have to be government annuity contracts for which the latter has to find funds. This is in the context of a major pay commission revision of salaries for the government sector, higher borrowings by the government to bridge the same, huge fertilizer and oil subsidy this year and the splurge that will happen in an election year as government machinery is fully used for this purpose (Indian general election is due in February/March 09 and many state elections are underway). Falling oil prices and commodity prices will help mitigate the deficit pressure.

The government has upped the cap on the amount foreign institutional investors can invest in treasury securities and the cash holding of the long only funds in India is finding its way to these as reflected by the constantly falling yields. Future flows are a function of how the global liquidity and risk appetite shapes up given the various uncertainties currently prevailing.

7. The export sector – IT, textiles, Diamonds Gems & Jewelery etc. have their fates tied to how the US and European economies and consumption shapes up. While rupee depreciation might appear favorable, cost pressures of importers and low demand will only put pressures on margin.

Some of the cash rich IT companies might provide deferred credit to their customers especially in most affected sectors with a view that when things settle down the relationship will be cemented further and provide much larger opportunities. While prima facie this is logical it does increase the risk profile of these companies substantially and if the expected stabilization does not happen in the time frame envisaged this could be good money after bad money.

8. Insurance companies that were supporting the market in a big way are finding that inflows have slowed substantially and there are policy lapses especially in the market linked policies called ULIP. The insurance industry is definitely in for a consolidation. In fact grape wine has that one of the major private sector insurers is showing huge losses in its portfolio and may require capital infusion shortly.

9. Job losses will be a reality given this scenario. Foreign companies have already started the process. Apart from this salary cuts have already been initiated. And those looking for jobs are going to find it hard to come by. While job loss estimates is politically sensitive and not published, real estate and textile – two of the major employers are indicating over one and a half million job cuts.

10. Hot money that normally moves the market in a significant way will be hard to come by. Apart from the various external reasons I have explained in my previous posts it reported that India specific hedge funds have done the worst. According to a report complied by Eurekahedge, a leading global hedge fund researcher, while the year-to-date losses of hedge funds across regions and strategies is only 12 per cent, India-specific funds have grossly underperformed, with a 53 per cent loss.

Eastern Europe and Russian funds, with 47 per cent loss, are the second worst performers. The performance of India-specific hedge funds compares poorly with other hedge funds in the Asian region too whose returns range between 13 and 25 per cent.

So investors with emerging markets as a destination through hedge fund vehicle (if it still does exist) will be hard to come by.

Add to this that the GDP growth estimate which in January was about 9% is now at 5 to 6%. Every analyst and economist has a figure to bandy and I’ am sure no body has an inkling of how they arrived at this figure except as a guesstimate. As I see it while Dalal Street has seen the pain the main streets are going to feel it only now. Given the Indian demography where nearly two- thirds of its population is below the age of 35, and nearly 50 % is below 25 and employable, while on the one side one can talk about a demographic dividend, any major fall in GDP and consequent job losses can be disastrous and will require out of the box approach to handle it.

Safety rule for now: Don’t be taken in by the breeze that may follow. You may want to enjoy it while it lasts but move out before the gale comes again. Err on the side of caution.

Disclosure: No stocks discussed - No stock position

Copyright © 2008 Tradesense

These are once in a century kind of events. To understand this better let’s take the period post the great depression. When things started looking up finally, having been bruised badly, the conservative mindset was dominant. So at any slight sign of excess players would unwind and reduce the risk quickly. This helped in more sustainable move up with much lesser volatility and uncertainty. But as years passed and a new set of players came – those who had not seen or felt the pains of the past and were witness only to the better times had a different risk profile and were willing to take greater risks. However they had the advantage of hearing firsthand about the depression and its related consequences. So, while the scale of movement on the up and down increased, their minds were also tempered by what they had heard and read much more than would the next set of generations. With time as new generation of players came who were much more distanced from the past pains and their risk appetites kept increasing. It cumulated over time to reach a level that now can be considered as the tilting point. So here we are. We would now see a number of changes that in the opinion of the wise in the governments and the intellectuals they call upon, is a safer environment to conduct business. I have elaborated this theme in my previous posts and ‘am not elaborating it any further.

So where does India stand in this? India has integrated with world economy in the past five years so much more rapidly than it did the decade prior to it. The kind of move that the Indian stock market made on the up was due to cheap money that came from sources outside India. Hence any major shifts in the environment in those markets which originated this cheap money are going to impact the Indian markets as severely. However well Indian companies do there will be no bull market without money flow in volumes.

Let’s look at some of the fundamental pointers which tell us that India shall be shaping up in close correlation to how the new world economic order evolves. Keep in mind that India’s external trade already constitutes over 40% of its GDP. Net investments by FIIs (Foreign Institutional Investors) in Indian stock exchanges by January 2008 were USD65 billion. In the last four years India has received USD50 billion as FDI (Foreign Direct Investment).

1. Rupee has depreciated against dollar to its lowest ever in its history (more than INR50 to a USD – a 27% depreciation YTD). This is lower than in 1991-92 when India pledged gold with Bank of England for getting a foreign currency line to fund its imports – which to me is the low this country saw in its financial history.

2. The kind of action that RBI and finance ministry has taken to ease liquidity and interest rate in the past four weeks is unprecedented. About INR2trn. (USD40bn.) was released into the system in a period of 3 weeks. The RBI has even gone ahead and approved lower risk weight age and changed the delinquency or NPA recognition standards for sectors such as real estate and infrastructure thus aiding bank balance sheet manipulation. This shows desperation and one has to read in between to understand where we stand. Despite such huge moves the money flow is still stagnant and the markets are only seeing downward pressure. It would probably have worked if the issues were India specific which is not the case.

3. The corporate leverage is the highest ever. When you listen to bank chairman saying companies do not want to take further leverage on their books and are not drawing down funds you it becomes clear that the company’s major business risks ahead therefore do not want a double whammy of financial risk also to take them down.

4. And where the companies are willing to take debt banks seem to become risk averse and are not lending. Most small and medium enterprises, which comprise of more than 40% of production output, are a victim. Banks also fear a fairly large write-off in this segment and hence do not good money to become bad.

5. The real estate sector which was the leader in the last up move is in dire straits. Some of the highly leveraged high profile companies have put many of the large projects on the block as debt repayments are due in the next six months to one year and there is little hope of rollover. Most real estate companies did not participate in Friday’s up move reflecting this. This sector will have to change its business model and the land bank game is a goner. Don’t expect to see any major up move in land prices for some time as many of them move to the auction block.

6. Infrastructure companies also had leveraged themselves highly as the government moved to the BOOT and BOT models. Now with scarcity of capital and high cost most projects will have to be government annuity contracts for which the latter has to find funds. This is in the context of a major pay commission revision of salaries for the government sector, higher borrowings by the government to bridge the same, huge fertilizer and oil subsidy this year and the splurge that will happen in an election year as government machinery is fully used for this purpose (Indian general election is due in February/March 09 and many state elections are underway). Falling oil prices and commodity prices will help mitigate the deficit pressure.

The government has upped the cap on the amount foreign institutional investors can invest in treasury securities and the cash holding of the long only funds in India is finding its way to these as reflected by the constantly falling yields. Future flows are a function of how the global liquidity and risk appetite shapes up given the various uncertainties currently prevailing.

7. The export sector – IT, textiles, Diamonds Gems & Jewelery etc. have their fates tied to how the US and European economies and consumption shapes up. While rupee depreciation might appear favorable, cost pressures of importers and low demand will only put pressures on margin.

Some of the cash rich IT companies might provide deferred credit to their customers especially in most affected sectors with a view that when things settle down the relationship will be cemented further and provide much larger opportunities. While prima facie this is logical it does increase the risk profile of these companies substantially and if the expected stabilization does not happen in the time frame envisaged this could be good money after bad money.

8. Insurance companies that were supporting the market in a big way are finding that inflows have slowed substantially and there are policy lapses especially in the market linked policies called ULIP. The insurance industry is definitely in for a consolidation. In fact grape wine has that one of the major private sector insurers is showing huge losses in its portfolio and may require capital infusion shortly.

9. Job losses will be a reality given this scenario. Foreign companies have already started the process. Apart from this salary cuts have already been initiated. And those looking for jobs are going to find it hard to come by. While job loss estimates is politically sensitive and not published, real estate and textile – two of the major employers are indicating over one and a half million job cuts.

10. Hot money that normally moves the market in a significant way will be hard to come by. Apart from the various external reasons I have explained in my previous posts it reported that India specific hedge funds have done the worst. According to a report complied by Eurekahedge, a leading global hedge fund researcher, while the year-to-date losses of hedge funds across regions and strategies is only 12 per cent, India-specific funds have grossly underperformed, with a 53 per cent loss.

Eastern Europe and Russian funds, with 47 per cent loss, are the second worst performers. The performance of India-specific hedge funds compares poorly with other hedge funds in the Asian region too whose returns range between 13 and 25 per cent.

So investors with emerging markets as a destination through hedge fund vehicle (if it still does exist) will be hard to come by.

Add to this that the GDP growth estimate which in January was about 9% is now at 5 to 6%. Every analyst and economist has a figure to bandy and I’ am sure no body has an inkling of how they arrived at this figure except as a guesstimate. As I see it while Dalal Street has seen the pain the main streets are going to feel it only now. Given the Indian demography where nearly two- thirds of its population is below the age of 35, and nearly 50 % is below 25 and employable, while on the one side one can talk about a demographic dividend, any major fall in GDP and consequent job losses can be disastrous and will require out of the box approach to handle it.

Safety rule for now: Don’t be taken in by the breeze that may follow. You may want to enjoy it while it lasts but move out before the gale comes again. Err on the side of caution.

Disclosure: No stocks discussed - No stock position

Copyright © 2008 Tradesense

No comments:

Post a Comment

Look forward to your views/comments.