It has been a while since I posted – was caught up in some personal issues and could not put my thoughts down. Having discussed many of the current hot issues including China before, it is becoming difficult to keep turning the same wheel again and again which many seem to be adept in doing. Let’s anyway look at some of the current concerns many of which were discussed earlier and then take a view.

As regards China it was identified in May 09 itself that:

…China doesn’t have the kind of social safety net one sees in the developed world, so it needs to keep its economy going at any cost. Millions of people have migrated to its cities, and now they’re hungry and unemployed. People without food or work tend to riot; to keep that from happening, the government is more than willing to artificially stimulate the economy, in the hopes of buying time until the global system re-stabilizes.

It’s literally forcing banks to lend - which will create a huge pile of horrible loans on top of the ones they’ve originated over the last decade (though of course we can’t see them). Don’t confuse fast growth with sustainable growth. As I’ve discussed in the past, China is suffering from Late Stage Growth Obesity. A not-inconsequential part of the tremendous growth it’s seen over the last 10 years came from lending to the US. Additionally, the quality of late-period growth was, in all likelihood, very poor, and the country now suffers from real overcapacity.

Identifying bubbles is a lot easier that timing their collapse. But as we’ve recently learned, you can defy the laws of financial gravity for only so long. Put simply, mean reversion is a bitch. And the longer inflated prices persist, the harder they fall when financial gravity brings them back to earth.”

It was also noted in early June 09 that:

…However, if there is to be a risk of a credit crisis in the future in China, similar to the one that has unfolded in the United States and Europe, the country would need to lack any other possible engine of growth.

In the United States and Europe, if credit had not outpaced incomes, growth would have been close to potential growth, i.e., in view of productivity gains and growth in the working-age population, around 2.25% in the United States, 1% in the United Kingdom and 1% in the euro zone. Credit was used to ensure more robust growth than would otherwise have been recorded.

In China, the current economic recovery is driven by credit; but there are exceptional circumstances with, for instance, the decline in China’s exports due to the contraction in global trade.

In a normal regime, productivity gains are high and potential growth is robust in China, and this rules out the need for a durable increase in indebtedness to stimulate growth.

However, it may well be that the current vigorous upturn in credit, driven by the government’s instructions, with loans extended at very favorable conditions for borrowers, could lead to the reappearance of non-performing loans in banks’ balance sheets, and the Chinese government will likely have to pay for them in the future as it already has done in the past.

And in January 09 it observed that:

The $584bn.China stimulus is expected to start having some impact from the second quarter. But the main factor would be the expected revival of the western markets after the second quarter which would then give a fillip back to Chinese exports. If this for some reason does not happen or is delayed than we may see some serious dumping by China causing prices worldwide to fall and adding to the deflationary trend. This could lead to protectionist tendencies to increase leading to a global slowdown in trade with attendant political and economic consequences.

As regards the market and FED it was observed in early May 09 that:

…The feel good factor is back. Many experts opine that we have indeed put in a bottom and that with due corrections we shall now march upwards. The fact that most were talking about a recovery that would be shaped L, U, W etc., contrary to the expectations as markets usually do, many experts think the market in its wisdom has sought a V shaped recovery….

…This is not to say that some of the macro parameters have not improved. But this sharp move up of the market has its consequences. The increasing appetite for risk has seen the US 10 year yield move up to 3.2% and the mortgage rates are up from around 4.7% to around 5.2%. And as explained in a previous post sharp up moves in equities is going to make the treasury and the Fed’s trillions of borrowing more expensive pushing up the interest higher which will increase risk for taxpayers and the country dramatically. Hence while printing money the Fed and treasury have to do a fine balancing and that means the interest rates still needs to managed within reasonable levels. This is not going to be easy and is going to be a fine line to tread on, not knowing where the line is.

Now here is the catch. On the one hand this would mean funding the bailouts is going to be more and more difficult and expensive while on the other hand liquidity will find its way to other asset classes. While the short term shift in liquidity to stocks and other assets may move these markets, sooner than later the reality of high interest rates and the inability/difficulty of funding the bailouts other than through FED buying more and more treasuries (printing money or quantitative easing) will become apparent. This we have experienced many a times is a sure shot formula for asset prices to finally form a bubble and lo! we are back to square one.

To me the market players should not get euphoric with current move. The players shifting their liquidity to the market to create such sharp moves would be actually shooting at their own legs. A measured slow consolidation is required and sharp move in asset prices will put the medium to long term sustained recovery in jeopardy. This whole process will be time consuming – running into number of years and the market player’s own action on a collective basis of how they handle this liquidity is going to determine how long the markets may take to make a long term sustainable up move.

On why the seeds decoupling have been sown, it was observed in February 09 that:

…As I see the lessons learnt/being learnt during this severe downturn will have a lasting impact as these Asian countries now re-orient there industrial and fiscal policies to ensure that over dependence on exports is reduced in the years to come. Also trade within the region will now be a much greater focus as two of the most populous countries in the region ‘Chindia’ look to push their growth with policies that are much more domestic investment and consumption oriented. India always was domestic consumption story (save the IT and IT enabled services and Generic Pharmaceutical industry) and now can be regarded as a great advantage.

… the reorientation will be challenging and will take time – a decade or so. But as the US and European consumption story sees its twilight in years to come it is the Asian and some of the resource rich countries such as Brazil that will need to fill-in. And as this re-orientation sees initial success foreign capital (US and European savings) will start seeking these countries and the capital required to sustain a reasonable growth rate will find its way. The seeds for this shift – possibly a power shift too - appears to have been sown.

The point to be understood is that normal downturns/recessions happen due to businesses over investing and generally the interest rates shooting up (through central bank actions) because of inflationary concerns causing demand to ease. The overcapacity brings down prices and as inflationary concerns diminish the interest rate environment softens and we see demand picking up and capacity utilization also move northward indicating revival. The underlying money circulatory system or credit delivery generally remains in reasonable health, although specific concerns may be there.

However the genesis of the current downturn/recession is the failure of this underlying system of credit delivery and money circulation which has its own attendant consequences. The businesses and consumers got into trouble because what they thought was a given (within a certain flexibility band of size or amount and price of credit) suddenly found the ground dry and had to face tight liquidity situation and thereby cut production/purchases etc.

The former situation is akin to an organ or two malfunctioning and with some external medication which can reach the organs through the circulatory system and body’s other organs/systems responding in help, the health can be restored reasonably fast – V shaped recovery. But if the body’s circulatory system is itself damaged and is the cause for other organs malfunctioning it becomes a real challenge to restore the health of the person as the medication has to given directly to the organs in the hope that their improving condition would stimulate the circulatory system and thus the patient’s health can be restored. How this will pan out is difficult to say – L, W, U and hopefully not X.

As Washington Post notes:

“…Growth spurts can emerge, and it appears increasingly likely that the U.S. economy will grow at a solid pace in the second half of the year, as companies restock depleted inventories. But it is unclear what would come after that, given the ongoing restrictions on credit.

U.S. banks have sustained massive losses already, and a wave of soured commercial real estate loans threatens to further limit their ability to lend in the year ahead. A bigger problem looms outside of banks -- in credit markets, which account for vast chunks of mortgage lending, consumer loans and commercial real estate loans. This shadow banking system remains dysfunctional -- notwithstanding a slew of programs the Fed put in place to get it going again -- and no one is sure when or whether it will recover.

All that makes it more expensive for people or businesses to borrow money -- if they can get a loan at all -- which could serve as a powerful brake on any recovery.

"Credit fuels housing. It fuels consumer durable goods. It fuels business investment. It's in every part of the economy," ... "Credit makes recessions after a financial crisis longer, and all the signs are that [it] is happening this time as well."

…The financial crisis and recession are reversing a 30-year trend carrying Americans toward a high point in debt. The ratio of consumer debt to the nation's total economic output rose to 97 percent in the first quarter of this year from 45 percent in 1975.

Currently, Americans are saving more and paying down debt; the savings rate was 1.2 percent of disposable income in early 2008. By the second quarter of this year, that rose to 5.2 percent.

Every dollar that Americans save is one fewer dollar for consumption, which means less economic output. When the savings rate goes up by a percentage point, spending decreases by more than $100 billion…”

So what will bail out American, Chinese and other businesses that are so dependent on the US consumer? The answer to this is the growth of the merging market consumers. As noted above as the US consumer dependant economies focus more on internal consumption and make moves to improve the living standards of their populations through better infrastructure, creating more job opportunities etc., the demand for goods worldwide will start looking up over time. American businesses will have to position themselves to exploit this opportunity.

Remember what the US consumer saves has to find its way to businesses or consumers elsewhere. This capital will flow to where the growth opportunities are – the emerging markets. And as these markets start providing the depth in demand (because of sheer numbers and necessarily due to credit explosion in these countries), American businesses will find its footing in the scale that they were/are used to. This reversal of fortune is going to take a lot of time. US companies already established in these regions will be the first to experience this shift and those focused within the US will have to think globally.

Slowly the cycle will turn, but for now situation seems too challenging for comfort.

Disclosure: No Positions

Copyright © 2008-09 Tradesense

Monday, August 17, 2009

Saturday, June 20, 2009

Have Banks Learnt Anything From The Financial Crisis?

With so much water having flown after the financial crisis I was wondering if anything has really changed in the way the key banks do their business. I came across an interesting Natixis special report which threw light on this and I thought I should share some of the key aspects of this report for you to make the judgment.

-More regulated, and supervised by governments, especially as many banks are partially nationalized;

-Simpler, due to the disappearance of the demand for complex financial assets (ABS, structured products, complicated exotic options, etc.);

-More cautious about risk taking (reduction in risk limits, increased capital consumption, different compensation systems for trading floors, etc.).

-Many banks in the United States and in Europe have been recapitalized by governments, so much so that some of them are practically nationalized.

-All these banks have also benefited from debt issuance guaranteed by the government.

-The aid provided by governments has been accompanied by conditions, generally regarding the compensation of management, traders, etc. This also entails a reduction in the volume of risk operations (proprietary trading).

It is striking to see that, in the recent period, many banks would:

− On the one hand recapitalize, in order to comply with the conditions (stress-tests) set by governments;

− On the other hand repay governments, in order to no longer be subject to constraints affecting the way they run their business (Table 1). This is particularly striking in the United States.

-CDOs, as shown by the tightening in CDS spreads (Charts 2A and B);

-CDOs, as shown by the tightening in CDS spreads (Charts 2A and B);

It is therefore not true that investors will only be interested in simple assets going forward.

Global liquidity is extraordinarily abundant (Chart 5), due to the highly expansionary monetary policies conducted since the start of the crisis on top of the previous surge in official reserves.

As soon as investor risk aversion decreased, asset price bubbles reappeared: surge in emerging-country equities (Chart 6), rise in the oil price despite the situation of excess supply in the market (Charts 7A and B).

As soon as investor risk aversion decreased, asset price bubbles reappeared: surge in emerging-country equities (Chart 6), rise in the oil price despite the situation of excess supply in the market (Charts 7A and B).

This demonstrates:

This demonstrates:

-some banks have not changed their business model; (not wanting to learn from the previous experience).

-demand for complex financial assets has in reality remained brisk; (investors are still playing suckers).

-the excess liquidity is still causing asset price bubbles, which once more demonstrates the central banks’ responsibility in the financial chaos;(Central Banks are working hard to create another bubble).

Disclosure: No Positions

The report starts with a question:

What is normally expected to happen with finance after the crisis?

Consensus seems to be that after the crisis finance will be

-More regulated, and supervised by governments, especially as many banks are partially nationalized;

-Simpler, due to the disappearance of the demand for complex financial assets (ABS, structured products, complicated exotic options, etc.);

-More cautious about risk taking (reduction in risk limits, increased capital consumption, different compensation systems for trading floors, etc.).

But do the current developments reflect it? Let’s first look at existing background in which many banks are operating.

-Many banks in the United States and in Europe have been recapitalized by governments, so much so that some of them are practically nationalized.

-All these banks have also benefited from debt issuance guaranteed by the government.

-The aid provided by governments has been accompanied by conditions, generally regarding the compensation of management, traders, etc. This also entails a reduction in the volume of risk operations (proprietary trading).

It is striking to see that, in the recent period, many banks would:

− On the one hand recapitalize, in order to comply with the conditions (stress-tests) set by governments;

− On the other hand repay governments, in order to no longer be subject to constraints affecting the way they run their business (Table 1). This is particularly striking in the United States.

These banks in all likelihood want to return to an investment bank model close to the one seen before the crisis.

Table - 1

On 9 June the Treasury authorized 10 banks to repay the funds injected in the autumn of 2008 by the government, for a total amount of USD 68 bn.(Table2)

Table - 2

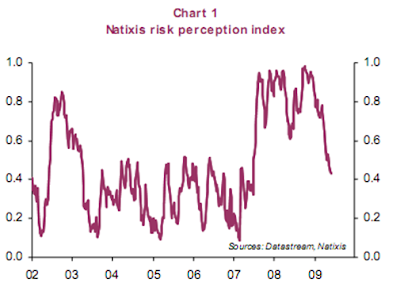

The recent period has been marked by a nose-dive in investor risk aversion (Chart 1), and, without delay, a return of demand for complex (toxic) assets, a demand that was believed to have disappeared for good:

-CDOs, as shown by the tightening in CDS spreads (Charts 2A and B);-CLOs, as shown by the rise in the prices of leveraged loans (Chart 3); etc.

It is therefore not true that investors will only be interested in simple assets going forward.

Global liquidity is extraordinarily abundant (Chart 5), due to the highly expansionary monetary policies conducted since the start of the crisis on top of the previous surge in official reserves.

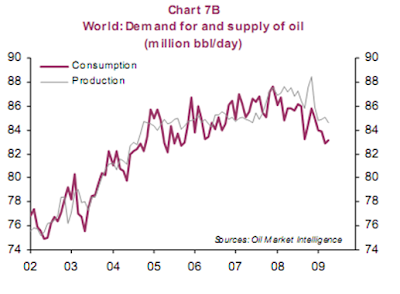

As soon as investor risk aversion decreased, asset price bubbles reappeared: surge in emerging-country equities (Chart 6), rise in the oil price despite the situation of excess supply in the market (Charts 7A and B).This demonstrates: -some banks have not changed their business model; (not wanting to learn from the previous experience).

-demand for complex financial assets has in reality remained brisk; (investors are still playing suckers).

-the excess liquidity is still causing asset price bubbles, which once more demonstrates the central banks’ responsibility in the financial chaos;(Central Banks are working hard to create another bubble).

Amen.

Disclosure: No Positions

Copyright © 2008-09 Tradesense

Sunday, June 7, 2009

Why the US stock market is stalling?

That the US and the Global economy are moving towards stability has been indicated by the rising oil and base metal prices as well as the stock market performance from the middle of March09. The surprising jobs data at a job loss of 345k against a much higher expected number, while did reaffirm the fact that the US economy is moving back to normalcy, the stock market reaction which one would attribute to such a margin of surprise was missing. Clearly this seems to have some other implications which the players are factoring-in.

Explanations could be along these lines.

-Home prices appear to have hit bottom in some areas of the country, but construction remains weak.

-The auto industry and retailing remain in distress. The job market is likely to remain in the doldrums for many months.

-A home foreclosure crisis is growing … As more foreclosed properties land on markets, real estate prices are falling further, adding to the losses and uncertainties confronting banks.

-Wage growth has been stagnating even as gasoline and medical costs rise, putting pressure on household finances. Average hourly wages were 3.1 percent higher last month than they were in May 2008, but the month-to-month increases in April and May were just 0.1 percent, to a seasonally adjusted $18.54, from $18.52, according to the Labor Department. Wages for manufacturing workers fell 0.1 percent.

-The jobs report presented a statistical puzzle. After shedding an average of more than 700,000 jobs each month during the first quarter, the economy lost 504,000 jobs in April, according to revised data, and the number was smaller still in May. Yet the unemployment rate leapt from an already high 8.9 percent, reinforcing fears it would reach double digits.

This disconnect owes to the way in which the government collects data. The number of jobs comes from a survey of employers, while the unemployment data is derived from a survey of households. In April and May, the number of people who told surveyors they were actively looking for work increased by more than one million. These people would have previously been considered outside the work force and thus excluded from the unemployment calculation. Now, they are officially back in the hunt, yet struggling to secure work.”

And to me this discomfort comes from the rising treasury yields. Says a NYT report

“The Treasury’s benchmark 10-year note fell 30/32, to 94 7/32, as investors edged away from buying government debt in the face of exploding federal deficits.

The yield, which moves in the opposite direction from the price, rose to 3.83 percent, from 3.71 percent late Thursday, and was up from 3.46 percent a week ago.

The creep toward higher interest rates represents a return to normalcy in some ways…

But higher interest rates on Treasuries make it more expensive for the government to borrow trillions in new debt, and they also raise mortgage rates for home buyers, threatening the government’s efforts to keep borrowing costs low.

But higher interest rates on Treasuries make it more expensive for the government to borrow trillions in new debt, and they also raise mortgage rates for home buyers, threatening the government’s efforts to keep borrowing costs low.”

This is something I have mentioned in my previous post as a key risk for the US market and is now emerging an important headwind.

A Miller Tabak + Co., LLC report brings out the concerns even more clearly:

“The action in the two year note today where the yield is up a dramatic 30 bps to 1.25%, the highest since mid November, is happening coincident with a move higher in yield in the fed funds futures contracts where the market has somewhat reset their expectations of what the Fed will do. The fed funds futures are pricing in a 48% chance of a 25 bps rate hike by the September 09 meeting and that is up from a 2% chance priced in just yesterday.

After today’s better than expected payroll figure being the main catalyst for today’s action in conjunction with the ever growing inflation concerns, the Fed needs to decipher what is a readjustment of growth expectations and/or what is related to inflation concerns and whether they will fight these trends in order to keep interest rates low.

Reading comments from Fed President and voting member of the FOMC Yellen within the past 15 minutes does not give much confidence that they know what’s going on and it seems that they had very little of a game plan going into their QE policy. Using quotes from DJ, she said that while buying MBS and US treasuries got off to a good start with yields heading lower, “there’s a lot that central bankers don’t know about the magnitude and duration of the effects of these policies” and “our standard monetary policy models do not incorporate financial frictions that lead to asset purchases having real effects.” She went on to say “we lack both the data and theory to provide strong guidance on these policies” and “we are sailing in uncharted waters, marking our maps with every bit of information along the way.” Yellen is a career economist and ex school professor so she’s learning first hand what its like to mess with the market. I’m worried if other Fed members are this uncertain.”

Fed not knowing what it is up to is a concern expressed before.

Another commentator albeit in a different context brings home the point regarding the long term yields.

“Listen, what really matters to energy prices these days is the perceived value of the dollar and the perceived ability of the government to stop its massive spending binge. Oil has been moving because of the disturbing widening of the yield curve that seemed to suggest that the government’s ability to keep rates down in the long end would make every dollar the government spends that they do not have more and more expensive to pay back. Oil moved because it saw the threat posed by the widening yield curve and it expressed those concerns with soaring gold and silver prices, ratcheting up copper prices. Not to mention talk in recent weeks that the untarnished best in the universe debt rating of the United States of America’s was even rumored to be downgraded.

And you Mr. Grumpy Bernanke have to go ruin it all by saying enough is enough. Why tell the Senate and Obama and the rest of America that we can’t have our cake and eat it too? I like cake! Don’t tell us that we cannot have it all like universal health care, finance Social Security, buy out auto companies, bail out Fannie and Freddie, massive stimulus packages and speculating in the green energy space and at the same time drive down the dollar and make commodity speculators rich. What kind of downer talk is that? Whenever you think that way remember there has never been anything false about hope. We have faced down impossible odds. We've been told that we're not ready, or that we shouldn't try, or that we can't afford it because our budget deficits threaten financial stability or we can’t because of our threatened ability to borrow indefinitely to fund a budget deficit that already this year is estimated to be $1.85 trillion, equivalent to 13 percent of the nation’s GDP the highest level since World War II. Or that we can’t because we are on path that will make this country bankrupt, just remember that generations of Americans have responded with a simple creed that sums up the spirit of a people. Yes we can! Yes we can! Commodity bulls all over the world thank you.”

Assuming the US authorities do get their exit strategy right and is able to balance the rate vs. growth concerns - will the global developments allow this to happen? To me it looks extremely difficult. According to a Natixix special report:

“The rise in long-term interest rates (particularly in the United States) is very bad news, since a fall in long-term interest rates was the only policy left for central banks.

What accounts for this rise?

− Inflationary risk due to the scale of monetary creation? But if expected inflation rises, there is no real inflation risk and, moreover, the US and European economies will remain very weak for a long time to come;

− Crowding-out effects due to the size of the expected public debts? But private indebtedness continues to fall and the savings rates keeps rising;

− Contagion from higher returns that can now be obtained, for instance on emerging-country equities, due to the economic recovery in Asia?

This third argument (correlation of bond yields in the United States and Europe with returns on other financial assets) seems the most reasonable in our view; it corresponds to a return of capital flows to emerging countries.”

And will emerging countries be able provide a much higher sustained returns to keep this flow sustained. To me this looks a possibility although it does tread into the decoupling argument which I had dealt in a previous post.

Natixix looks at China’s ability to sustain a 9%+ growth on the following lines. In the context of the growth in credit in China (which can be applied to many large emerging economies) it says:

“…However, if there is to be a risk of a credit crisis in the future in China, similar to the one that has unfolded in the United States and Europe, the country would need to lack any other possible engine of growth.

In the United States and Europe, if credit had not outpaced incomes, growth would have been close to potential growth, i.e., in view of productivity gains and growth in the working-age population, around 2.25% in the United States, 1% in the United Kingdom and 1% in the euro zone. Credit was used to ensure more robust growth than would otherwise have been recorded.

On the other hand:

“Productivity gains, in China, are accounted for by what are normal factors in an emerging country:

− Migration from the countryside into cities, as the productivity of migrants improves significantly, as is reflected by the income differential between cities and the countryside;

−Very high level of investment;

− Technology transfers via direct investment.

…growth can be estimated at 9% per year at least. There is accordingly no reason why it would be necessary, in a normal situation, to boost demand by credit in China, and this in fact explains the medium-term stability of the credit-to-GDP ratio in China...

...The causes of productivity gains in China are durable, and this implies that potential growth will remain robust for a long time, resulting in a situation where there is no long-run need for a sharp rise in debt ratios.

In the United States and Europe, the low level of potential growth in comparison with the robust growth one wants to achieve has led to a steep rise in debt ratios being used, and this sparked the crisis because of excess indebtedness.

In China, the current economic recovery is driven by credit; but there are exceptional circumstances with, for instance, the decline in China’s exports due to the contraction in global trade.

In a normal regime, productivity gains are high and potential growth is robust in China, and this rules out the need for a durable increase in indebtedness to stimulate growth.

However, it may well be that the current vigorous upturn in credit, driven by the government’s instructions, with loans extended at very favorable conditions for borrowers, could lead to the reappearance of non-performing loans in banks’ balance sheets, and the Chinese government will likely have to pay for them in the future as it already has done in the past.” (US & Europe are no different).

Disclosure: No Positions

Copyright © 2008-09 Tradesense

Explanations could be along these lines.

-Home prices appear to have hit bottom in some areas of the country, but construction remains weak.

-The auto industry and retailing remain in distress. The job market is likely to remain in the doldrums for many months.

-A home foreclosure crisis is growing … As more foreclosed properties land on markets, real estate prices are falling further, adding to the losses and uncertainties confronting banks.

-Wage growth has been stagnating even as gasoline and medical costs rise, putting pressure on household finances. Average hourly wages were 3.1 percent higher last month than they were in May 2008, but the month-to-month increases in April and May were just 0.1 percent, to a seasonally adjusted $18.54, from $18.52, according to the Labor Department. Wages for manufacturing workers fell 0.1 percent.

-The jobs report presented a statistical puzzle. After shedding an average of more than 700,000 jobs each month during the first quarter, the economy lost 504,000 jobs in April, according to revised data, and the number was smaller still in May. Yet the unemployment rate leapt from an already high 8.9 percent, reinforcing fears it would reach double digits.

This disconnect owes to the way in which the government collects data. The number of jobs comes from a survey of employers, while the unemployment data is derived from a survey of households. In April and May, the number of people who told surveyors they were actively looking for work increased by more than one million. These people would have previously been considered outside the work force and thus excluded from the unemployment calculation. Now, they are officially back in the hunt, yet struggling to secure work.”

And to me this discomfort comes from the rising treasury yields. Says a NYT report

“The Treasury’s benchmark 10-year note fell 30/32, to 94 7/32, as investors edged away from buying government debt in the face of exploding federal deficits.

The yield, which moves in the opposite direction from the price, rose to 3.83 percent, from 3.71 percent late Thursday, and was up from 3.46 percent a week ago.

The creep toward higher interest rates represents a return to normalcy in some ways…

But higher interest rates on Treasuries make it more expensive for the government to borrow trillions in new debt, and they also raise mortgage rates for home buyers, threatening the government’s efforts to keep borrowing costs low.

But higher interest rates on Treasuries make it more expensive for the government to borrow trillions in new debt, and they also raise mortgage rates for home buyers, threatening the government’s efforts to keep borrowing costs low.”

This is something I have mentioned in my previous post as a key risk for the US market and is now emerging an important headwind.

A Miller Tabak + Co., LLC report brings out the concerns even more clearly:

“The action in the two year note today where the yield is up a dramatic 30 bps to 1.25%, the highest since mid November, is happening coincident with a move higher in yield in the fed funds futures contracts where the market has somewhat reset their expectations of what the Fed will do. The fed funds futures are pricing in a 48% chance of a 25 bps rate hike by the September 09 meeting and that is up from a 2% chance priced in just yesterday.

After today’s better than expected payroll figure being the main catalyst for today’s action in conjunction with the ever growing inflation concerns, the Fed needs to decipher what is a readjustment of growth expectations and/or what is related to inflation concerns and whether they will fight these trends in order to keep interest rates low.

Reading comments from Fed President and voting member of the FOMC Yellen within the past 15 minutes does not give much confidence that they know what’s going on and it seems that they had very little of a game plan going into their QE policy. Using quotes from DJ, she said that while buying MBS and US treasuries got off to a good start with yields heading lower, “there’s a lot that central bankers don’t know about the magnitude and duration of the effects of these policies” and “our standard monetary policy models do not incorporate financial frictions that lead to asset purchases having real effects.” She went on to say “we lack both the data and theory to provide strong guidance on these policies” and “we are sailing in uncharted waters, marking our maps with every bit of information along the way.” Yellen is a career economist and ex school professor so she’s learning first hand what its like to mess with the market. I’m worried if other Fed members are this uncertain.”

Fed not knowing what it is up to is a concern expressed before.

Another commentator albeit in a different context brings home the point regarding the long term yields.

“Listen, what really matters to energy prices these days is the perceived value of the dollar and the perceived ability of the government to stop its massive spending binge. Oil has been moving because of the disturbing widening of the yield curve that seemed to suggest that the government’s ability to keep rates down in the long end would make every dollar the government spends that they do not have more and more expensive to pay back. Oil moved because it saw the threat posed by the widening yield curve and it expressed those concerns with soaring gold and silver prices, ratcheting up copper prices. Not to mention talk in recent weeks that the untarnished best in the universe debt rating of the United States of America’s was even rumored to be downgraded.

And you Mr. Grumpy Bernanke have to go ruin it all by saying enough is enough. Why tell the Senate and Obama and the rest of America that we can’t have our cake and eat it too? I like cake! Don’t tell us that we cannot have it all like universal health care, finance Social Security, buy out auto companies, bail out Fannie and Freddie, massive stimulus packages and speculating in the green energy space and at the same time drive down the dollar and make commodity speculators rich. What kind of downer talk is that? Whenever you think that way remember there has never been anything false about hope. We have faced down impossible odds. We've been told that we're not ready, or that we shouldn't try, or that we can't afford it because our budget deficits threaten financial stability or we can’t because of our threatened ability to borrow indefinitely to fund a budget deficit that already this year is estimated to be $1.85 trillion, equivalent to 13 percent of the nation’s GDP the highest level since World War II. Or that we can’t because we are on path that will make this country bankrupt, just remember that generations of Americans have responded with a simple creed that sums up the spirit of a people. Yes we can! Yes we can! Commodity bulls all over the world thank you.”

Assuming the US authorities do get their exit strategy right and is able to balance the rate vs. growth concerns - will the global developments allow this to happen? To me it looks extremely difficult. According to a Natixix special report:

“The rise in long-term interest rates (particularly in the United States) is very bad news, since a fall in long-term interest rates was the only policy left for central banks.

What accounts for this rise?

− Inflationary risk due to the scale of monetary creation? But if expected inflation rises, there is no real inflation risk and, moreover, the US and European economies will remain very weak for a long time to come;

− Crowding-out effects due to the size of the expected public debts? But private indebtedness continues to fall and the savings rates keeps rising;

− Contagion from higher returns that can now be obtained, for instance on emerging-country equities, due to the economic recovery in Asia?

This third argument (correlation of bond yields in the United States and Europe with returns on other financial assets) seems the most reasonable in our view; it corresponds to a return of capital flows to emerging countries.”

And will emerging countries be able provide a much higher sustained returns to keep this flow sustained. To me this looks a possibility although it does tread into the decoupling argument which I had dealt in a previous post.

Natixix looks at China’s ability to sustain a 9%+ growth on the following lines. In the context of the growth in credit in China (which can be applied to many large emerging economies) it says:

“…However, if there is to be a risk of a credit crisis in the future in China, similar to the one that has unfolded in the United States and Europe, the country would need to lack any other possible engine of growth.

In the United States and Europe, if credit had not outpaced incomes, growth would have been close to potential growth, i.e., in view of productivity gains and growth in the working-age population, around 2.25% in the United States, 1% in the United Kingdom and 1% in the euro zone. Credit was used to ensure more robust growth than would otherwise have been recorded.

On the other hand:

“Productivity gains, in China, are accounted for by what are normal factors in an emerging country:

− Migration from the countryside into cities, as the productivity of migrants improves significantly, as is reflected by the income differential between cities and the countryside;

−Very high level of investment;

− Technology transfers via direct investment.

…growth can be estimated at 9% per year at least. There is accordingly no reason why it would be necessary, in a normal situation, to boost demand by credit in China, and this in fact explains the medium-term stability of the credit-to-GDP ratio in China...

...The causes of productivity gains in China are durable, and this implies that potential growth will remain robust for a long time, resulting in a situation where there is no long-run need for a sharp rise in debt ratios.

In the United States and Europe, the low level of potential growth in comparison with the robust growth one wants to achieve has led to a steep rise in debt ratios being used, and this sparked the crisis because of excess indebtedness.

In China, the current economic recovery is driven by credit; but there are exceptional circumstances with, for instance, the decline in China’s exports due to the contraction in global trade.

In a normal regime, productivity gains are high and potential growth is robust in China, and this rules out the need for a durable increase in indebtedness to stimulate growth.

However, it may well be that the current vigorous upturn in credit, driven by the government’s instructions, with loans extended at very favorable conditions for borrowers, could lead to the reappearance of non-performing loans in banks’ balance sheets, and the Chinese government will likely have to pay for them in the future as it already has done in the past.” (US & Europe are no different).

Disclosure: No Positions

Copyright © 2008-09 Tradesense

Sunday, May 10, 2009

Stress Test For The Street

Funny are the ways of Street…but street is most honorable…and it cannot be wrong…never fight Mr. Market. If you do you would be mauled. But in 2007 those who went against the street benefitted the most. The street does loose its head and there are those phases when not all the facts/news is factored-in. The art is to figure out as to when Mr. Market would look to redeem the honor. This becomes all the more difficult when the stakes of the mighty are involved and for some period they are able to manage the street to their ways. With the bank stress test climax the stress test for the street has begun.

NYT reports

"A day after the bank stress tests were released, two major institutions, Wells Fargo and Morgan Stanley, handily raised billions of dollars in the capital markets on Friday to satisfy new federal demands for more capital. A third, Bank of America, hastily laid out plans to sell billions of dollars in new stock.

The speed and ease with which the banks swung into action, combined with a surge in financial shares, was hailed as a sign that confidence was returning to the financial industry. The sales seemed to put to rest questions about whether big banks would be able to lure private investors, rather than have to turn to the government again.

Before the results were made public, many of the larger banks successfully pushed the government to minimize the capital they needed to raise.

…With some off to such a rapid start — Goldman Sachs raised $5 billion before the stress test results were announced — the race is now on among the most robust to repay the government money they received last fall and so escape from government control. "

Copyright © 2008-09 Tradesense

NYT reports

"A day after the bank stress tests were released, two major institutions, Wells Fargo and Morgan Stanley, handily raised billions of dollars in the capital markets on Friday to satisfy new federal demands for more capital. A third, Bank of America, hastily laid out plans to sell billions of dollars in new stock.

The speed and ease with which the banks swung into action, combined with a surge in financial shares, was hailed as a sign that confidence was returning to the financial industry. The sales seemed to put to rest questions about whether big banks would be able to lure private investors, rather than have to turn to the government again.

Before the results were made public, many of the larger banks successfully pushed the government to minimize the capital they needed to raise.

…With some off to such a rapid start — Goldman Sachs raised $5 billion before the stress test results were announced — the race is now on among the most robust to repay the government money they received last fall and so escape from government control. "

Most probably they not want to loose the control over the government?

The script which I mentioned in my previous post is unfolding further. The models and inputs, it is understood were provided by the industry and it is understood that the inputs for the test were not independently checked for its veracity thoroughly. 180 examiners examining 19 banks, many with very large and global operations over eight weeks could have seen only what the banks wanted them to show. Anyone who has worked in bank operations would vouch for that. And the icing was that the banks could negotiate the capital it required! Further the scenarios for which the banks assets were stressed were according to keen observers, was a little too optimistic. Also the fact that there were leaks which now match the actual also lend credence to this stage management. It would be good to find out as to who invested in the bank issues. The quirky feeling is that TARP money in getting circulated indirectly. Competitors holding hands for a cause!

The NYT report quotes Meredith Whitney:

"But Meredith A. Whitney, a prominent banking analyst, said the results underscored the difficulties banks faced.

“The revenue environment is very different,” Ms. Whitney said. Given the recession, banks are not going to make much money from credit cards or originating mortgages, she said. And even if all the banks secured more capital, they still might not lend, holding back the economy."

The same report says:

"Despite the sobering outlook, the mood on Wall Street was generally upbeat after the rosier-than-expected assessment of the biggest banks. The stock market climbed, with the Standard & Poor’s 500-stock index gaining 2.4 percent on Friday.

“If there were holes in this, the market would have seen it,” said Stuart Plesser, an analyst at Standard & Poor’s."

I wish the market had seen the coming of sub-prime in 2005-06 and the rating agencies it appears are never going to learn! Or probably they are also the part of script!!

To me all this is blind (Treasury & Fed) leading other blinds (banks) in the hope that miraculously both will suddenly find vision. First part has been enacted to make the audience (street) believe that both indeed have sight. How far these players are willing to take this make-belief is anybody’s guess. To me the stress test for the street has only begun.

For the sake of so many retail investors I do hope that the miracle does happen.

Disclosure: No Positions

Copyright © 2008-09 Tradesense

Sunday, May 3, 2009

Manipulonomics

The feel good factor is back. Many experts opine that we have indeed put in a bottom and that with due corrections we shall now march upwards. The fact that most were talking about a recovery that would be shaped L, U, W etc., contrary to the expectations as markets usually do, many experts think the market in its wisdom has sought a V shaped recovery. Even the bulls have been taken by surprise at the swiftness and the ease of the up move. What started as a short covering in financials following the leak of Citi’s internal memo stating profitable operations with BOA backing it up and Wells Fargo following it up with a pre-result announcement it appeared a well coordinated effort. And then there was this panic that set in – panic buying. To me this appeared a well prepared script. When you have to move anything heavy say a huge log, the initial efforts are huge and once it rolls, it rolls with slight push thereafter. Once the shorts covered, the institutions which have their hearts in their hands and have been funded by taxpayers’ bonanza needed that the market cut back its negative bias were probably instructed to move it. Sentiment is a great player in how things shape up and to prop it up surely the main focus. Once moved there were others who had their urge to take risk and the scampering started?

This is not to say that some of the macro parameters have not improved. But this sharp move up of the market has has its consequences. The increasing appetite for risk has seen the US 10 year yield move up to 3.2% and the mortgage rates are up from around 4.7% to around 5.2%. And as explained in a previous post sharp up moves in equities is going to make the treasury and the Fed’s trillions of borrowing more expensive pushing up the interest higher which will increase risk for taxpayers and the country dramatically. Hence while printing money the Fed and treasury have to do a fine balancing and that means the interest rates still needs to managed within reasonable levels. This is not going to be easy and is going to be a fine line to tread on, not knowing where the line is.

Prechter explaining his logic for Dow 1000 says:

“The primary reason I believe the Dow is going to fall that far is its Elliott wave structure, which calls for it. But I can also see a monetary reason for this event. The tremendous inflation of the past 76 years has occurred primarily by way of instrument of credit, not banknotes. Credit can implode.

The only monetary outcome that will make sense of the Elliott wave structure is for the market value of dollar-denominated credit to shrink by over 90 percent. Given the eroded state of capital goods in the U.S. and the depletion of manufacturing capacity, it is not hard to see why all these IOUs have a deteriorating basis of repayment. The future has already been fully mortgaged; it's time to pay. But there is no money to pay, only more IOUs, which cannot be paid, either. So the credit supply (after a brief respite) will continue to shrink, which means that wealth, and therefore purchasing power, will disappear along with it. In the broadest sense, this change will constitute a collapse in the "money supply."

Apart from the sentiment angle there seems to be another perspective. The results of the bank stress tests. It was quite clear to the authorities that post these results many of the banks will need to raise more capital. Given the coziness that they have with many of these big banks – (this interesting NYT piece brings it out) and that the lawmakers may not be very inclined to commit more tax payer dollars, the need for market sentiment to improve was a necessity. The postponement of the stress test results is a result of contention between the banks and the treasury/Fed according to reports.

Also Bloomberg reports:

“Miller, a former bank examiner, said his estimate assumes regulators will require banks to maintain tangible common equity, one of the most conservative measures of capital, equal to 4 percent of their risk-weighted assets over the next two years, to withstand losses in case the recession worsens. The tests, originally scheduled for release on May 4, are set to be disclosed after U.S. markets close on May 7, according to a government official who spoke on condition of anonymity.

Bank of America Corp., JPMorgan Chase & Co., Citigroup Inc. and the 16 other banks received preliminary results last week and have been debating the findings with regulators. Officials favor tangible common equity of about 4 percent of a bank’s assets and so-called Tier 1 capital worth about 6 percent, people familiar with the tests say. Tangible common equity, or TCE, is a gauge of financial strength that excludes intangibles such as trademarks that can’t be used to make payments. Tier 1 capital is a broader measure monitored by regulators.

“When you start talking about 4 percent on risk-weighted assets based on the stress test two years out, most banks will be required to raise more capital,” Miller said in an interview yesterday. “I believe it will be as high as 14.” He declined to name them.

Citigroup, which has already taken $45 billion in U.S. taxpayer funds to shore up its finances, may need to raise as much as $10 billion in new capital, the Wall Street Journal reported today, citing people familiar with the matter. Jon Diat, a spokesman for the New York-based bank, declined to comment.”

As one commentator pointed out that we are in the mess that we are due to various models for derivatives/securitization being used and now we are trying sort it out by another modeling exercise!! One has seen the efficacy of these exercises and of course the possibility that they may show what they believe should be, need not surprise.

Respected and well regarded investors also have very sharp points to make. Bloomberg reports:

“Berkshire Hathaway Inc. Vice Chairman Charles Munger, whose company is the largest private shareholder in Goldman Sachs Group Inc. and Wells Fargo & Co., said banks will use their “enormous political power” to prevent changes to the industry that would benefit society.

“This is an enormously influential group of people, and 90 percent of that influence is being spent to gain powers and practices that the world would be better off without,” Munger, 85, said yesterday in an interview with Bloomberg Television. “It will be very hard to accomplish the kind of surgery that would be desirable for the wider civilization.”

Munger said the financial companies spent $500 million on political contributions and lobbying efforts over the last decade. They have a “vested interest” in protecting the system as it exists because of the high levels of pay they were earning, he said. The five biggest U.S. securities firms, only two of which still exist as independent companies, paid their employees about $39 billion in bonuses in 2007.

“They would like to get back as closely as possible to business as usual, and they have enormous political power,” he said.”

There are some other very valid points of view that are difficult to ignore:

1. Since last fall, our financial wizards have promised $12.8 trillion in bailout funds to primarily well connected cronies. The US national debt since the birth of this great nation now stands at a comparable $11 trillion. None of these debts will ever be paid off and it’s hard to fathom how anyone believes to the contrary.

The Fed’s “balance sheet” is supposed to be the substance behind their issuance of money. This balance sheet has been comprised of smoke and mirrors for decades since the total fiat era started in 1973. Those days now look golden compared to the current makeup.

The Fed used to hold almost exclusively Treasury securities with which to perform their various “operations”. Only 24% of their holdings are now in Treasuries. The rest is a toxic soup that they’ve now taken on (mortgage backed securities, commercial paper, money market assets, failed crony paper, etc.) to keep the entire system afloat. The mortgage backed securities, for example, are really worth around 35% on the dollar. The Fed and other banks holding this junk assign pretend values of 100% on them.

The Fed balance sheet had more than doubled to $2.19 trillion since the global meltdown started. It looks like they took the “good bank – bad bank” scenario seriously but made the wrong choice. Watching the world’s most influential bank implode is a rare event.

Most local banks are FDIC insured. These banks also hold just over $200 trillion in obscure derivatives. The reserves to back up these positions are a mere 3.5% as opposed to a more normal 10% backing of solid and traditional loans. Banking gone wild.

More here…

2. The banks are back. Profits are up. Write downs are lower. The government has their back. And the worst is over.

Forget Swiss-based USB. Their huge losses were the exception…

Judging by their latest quarterly reports, big banks have finally figured out how to make money again.

Goldman Sachs, JPMorgan, Bank of America, Wells Fargo and even Citigroup all reported profits for the first quarter.

But a closer look under the hood reveals that many of the big banks reported fake earnings…

-Bank of America arbitrarily increased the value of its Merrill Lynch assets.

-Goldman Sachs bunched much of its losses into the month of December – a month it skipped reporting on this year.

JP Morgan’s bonds fell in price. And that perversely allowed the bank to increase its bottom line. This is how the New York Times explained it: “Theoretically, JP Morgan could retire them and buy them back at a cheaper price; that’s sort of like saying you’re richer because the value of your home has dropped.”

More here…

While China is being touted as a savior there is a very interesting point of view on the coming of a China bubble.

“China’s fortunes over the past decade remind me of Lucent Technologies in the 1990s. Lucent (now Alcatel-Lucent (ALU)) was selling equipment to dot-coms. At first, its growth was natural, the result of selling telecom equipment to traditional, cash-generating companies. Thereafter, it was only semi-natural: Dot-coms were able to buy Lucent’s equipment only by raising money through private equity and equity markets, since their business models didn’t factor in the necessity of cash-flow generation.

Funds to buy Lucent’s equipment therefore quickly dried up, and the company’s growth should have decelerated or declined. Instead, Lucent offered its own financing to dot-coms by borrowing and lending money on the cheap to finance the purchase of its own equipment. This worked well enough - until the time came to pay back the loans.

The US, of course, isn’t a dot-com. But a great portion of our growth came from borrowing Chinese money to buy Chinese goods - which means that Chinese growth was dependent on that very same borrowing.

Now the US (and the rest of the world) is retrenching, corporations are slashing their spending, consumers are having moments of sickening recognition - and the consumption of Chinese goods is on the decline. This is where my dot-com analogy breaks down. Unlike Lucent, China has nuclear weapon. It can print money at will, and can simply order its banks to lend; this is a communist-command economy, after all. Lucent is now a $2 stock - but China won’t go down that easily…

…China doesn’t have the kind of social safety net one sees in the developed world, so it needs to keep its economy going at any cost. Millions of people have migrated to its cities, and now they’re hungry and unemployed. People without food or work tend to riot; to keep that from happening, the government is more than willing to artificially stimulate the economy, in the hopes of buying time until the global system restabilizes.

It’s literally forcing banks to lend - which will create a huge pile of horrible loans on top of the ones they’ve originated over the last decade (though of course we can’t see them). Don’t confuse fast growth with sustainable growth. As I’ve discussed in the past, China is suffering from Late Stage Growth Obesity. A not-inconsequential part of the tremendous growth it’s seen over the last 10 years came from lending to the US. Additionally, the quality of late-period growth was, in all likelihood, very poor, and the country now suffers from real overcapacity.

Identifying bubbles is a lot easier that timing their collapse. But as we’ve recently learned, you can defy the laws of financial gravity for only so long. Put simply, mean reversion is a bitch. And the longer inflated prices persist, the harder they fall when financial gravity brings them back to earth.”

While many key indicators may be looking better the fact that the financial system will take a lot of effort and time to straighten out should not be lost sight of. How much ever smoke screen you create at some point the realities will surface with a lot of pain.

Disclosure: No Positions

Copyright © 2008-09 Tradesense

This is not to say that some of the macro parameters have not improved. But this sharp move up of the market has has its consequences. The increasing appetite for risk has seen the US 10 year yield move up to 3.2% and the mortgage rates are up from around 4.7% to around 5.2%. And as explained in a previous post sharp up moves in equities is going to make the treasury and the Fed’s trillions of borrowing more expensive pushing up the interest higher which will increase risk for taxpayers and the country dramatically. Hence while printing money the Fed and treasury have to do a fine balancing and that means the interest rates still needs to managed within reasonable levels. This is not going to be easy and is going to be a fine line to tread on, not knowing where the line is.

Prechter explaining his logic for Dow 1000 says:

“The primary reason I believe the Dow is going to fall that far is its Elliott wave structure, which calls for it. But I can also see a monetary reason for this event. The tremendous inflation of the past 76 years has occurred primarily by way of instrument of credit, not banknotes. Credit can implode.

The only monetary outcome that will make sense of the Elliott wave structure is for the market value of dollar-denominated credit to shrink by over 90 percent. Given the eroded state of capital goods in the U.S. and the depletion of manufacturing capacity, it is not hard to see why all these IOUs have a deteriorating basis of repayment. The future has already been fully mortgaged; it's time to pay. But there is no money to pay, only more IOUs, which cannot be paid, either. So the credit supply (after a brief respite) will continue to shrink, which means that wealth, and therefore purchasing power, will disappear along with it. In the broadest sense, this change will constitute a collapse in the "money supply."

Apart from the sentiment angle there seems to be another perspective. The results of the bank stress tests. It was quite clear to the authorities that post these results many of the banks will need to raise more capital. Given the coziness that they have with many of these big banks – (this interesting NYT piece brings it out) and that the lawmakers may not be very inclined to commit more tax payer dollars, the need for market sentiment to improve was a necessity. The postponement of the stress test results is a result of contention between the banks and the treasury/Fed according to reports.

Also Bloomberg reports:

“Miller, a former bank examiner, said his estimate assumes regulators will require banks to maintain tangible common equity, one of the most conservative measures of capital, equal to 4 percent of their risk-weighted assets over the next two years, to withstand losses in case the recession worsens. The tests, originally scheduled for release on May 4, are set to be disclosed after U.S. markets close on May 7, according to a government official who spoke on condition of anonymity.

Bank of America Corp., JPMorgan Chase & Co., Citigroup Inc. and the 16 other banks received preliminary results last week and have been debating the findings with regulators. Officials favor tangible common equity of about 4 percent of a bank’s assets and so-called Tier 1 capital worth about 6 percent, people familiar with the tests say. Tangible common equity, or TCE, is a gauge of financial strength that excludes intangibles such as trademarks that can’t be used to make payments. Tier 1 capital is a broader measure monitored by regulators.

“When you start talking about 4 percent on risk-weighted assets based on the stress test two years out, most banks will be required to raise more capital,” Miller said in an interview yesterday. “I believe it will be as high as 14.” He declined to name them.

Citigroup, which has already taken $45 billion in U.S. taxpayer funds to shore up its finances, may need to raise as much as $10 billion in new capital, the Wall Street Journal reported today, citing people familiar with the matter. Jon Diat, a spokesman for the New York-based bank, declined to comment.”

As one commentator pointed out that we are in the mess that we are due to various models for derivatives/securitization being used and now we are trying sort it out by another modeling exercise!! One has seen the efficacy of these exercises and of course the possibility that they may show what they believe should be, need not surprise.

Respected and well regarded investors also have very sharp points to make. Bloomberg reports:

“Berkshire Hathaway Inc. Vice Chairman Charles Munger, whose company is the largest private shareholder in Goldman Sachs Group Inc. and Wells Fargo & Co., said banks will use their “enormous political power” to prevent changes to the industry that would benefit society.

“This is an enormously influential group of people, and 90 percent of that influence is being spent to gain powers and practices that the world would be better off without,” Munger, 85, said yesterday in an interview with Bloomberg Television. “It will be very hard to accomplish the kind of surgery that would be desirable for the wider civilization.”

Munger said the financial companies spent $500 million on political contributions and lobbying efforts over the last decade. They have a “vested interest” in protecting the system as it exists because of the high levels of pay they were earning, he said. The five biggest U.S. securities firms, only two of which still exist as independent companies, paid their employees about $39 billion in bonuses in 2007.

“They would like to get back as closely as possible to business as usual, and they have enormous political power,” he said.”

There are some other very valid points of view that are difficult to ignore:

1. Since last fall, our financial wizards have promised $12.8 trillion in bailout funds to primarily well connected cronies. The US national debt since the birth of this great nation now stands at a comparable $11 trillion. None of these debts will ever be paid off and it’s hard to fathom how anyone believes to the contrary.

The Fed’s “balance sheet” is supposed to be the substance behind their issuance of money. This balance sheet has been comprised of smoke and mirrors for decades since the total fiat era started in 1973. Those days now look golden compared to the current makeup.

The Fed used to hold almost exclusively Treasury securities with which to perform their various “operations”. Only 24% of their holdings are now in Treasuries. The rest is a toxic soup that they’ve now taken on (mortgage backed securities, commercial paper, money market assets, failed crony paper, etc.) to keep the entire system afloat. The mortgage backed securities, for example, are really worth around 35% on the dollar. The Fed and other banks holding this junk assign pretend values of 100% on them.

The Fed balance sheet had more than doubled to $2.19 trillion since the global meltdown started. It looks like they took the “good bank – bad bank” scenario seriously but made the wrong choice. Watching the world’s most influential bank implode is a rare event.

Most local banks are FDIC insured. These banks also hold just over $200 trillion in obscure derivatives. The reserves to back up these positions are a mere 3.5% as opposed to a more normal 10% backing of solid and traditional loans. Banking gone wild.

More here…

2. The banks are back. Profits are up. Write downs are lower. The government has their back. And the worst is over.

Forget Swiss-based USB. Their huge losses were the exception…

Judging by their latest quarterly reports, big banks have finally figured out how to make money again.

Goldman Sachs, JPMorgan, Bank of America, Wells Fargo and even Citigroup all reported profits for the first quarter.

But a closer look under the hood reveals that many of the big banks reported fake earnings…

-Bank of America arbitrarily increased the value of its Merrill Lynch assets.

-Goldman Sachs bunched much of its losses into the month of December – a month it skipped reporting on this year.

JP Morgan’s bonds fell in price. And that perversely allowed the bank to increase its bottom line. This is how the New York Times explained it: “Theoretically, JP Morgan could retire them and buy them back at a cheaper price; that’s sort of like saying you’re richer because the value of your home has dropped.”

More here…

While China is being touted as a savior there is a very interesting point of view on the coming of a China bubble.

“China’s fortunes over the past decade remind me of Lucent Technologies in the 1990s. Lucent (now Alcatel-Lucent (ALU)) was selling equipment to dot-coms. At first, its growth was natural, the result of selling telecom equipment to traditional, cash-generating companies. Thereafter, it was only semi-natural: Dot-coms were able to buy Lucent’s equipment only by raising money through private equity and equity markets, since their business models didn’t factor in the necessity of cash-flow generation.

Funds to buy Lucent’s equipment therefore quickly dried up, and the company’s growth should have decelerated or declined. Instead, Lucent offered its own financing to dot-coms by borrowing and lending money on the cheap to finance the purchase of its own equipment. This worked well enough - until the time came to pay back the loans.

The US, of course, isn’t a dot-com. But a great portion of our growth came from borrowing Chinese money to buy Chinese goods - which means that Chinese growth was dependent on that very same borrowing.

Now the US (and the rest of the world) is retrenching, corporations are slashing their spending, consumers are having moments of sickening recognition - and the consumption of Chinese goods is on the decline. This is where my dot-com analogy breaks down. Unlike Lucent, China has nuclear weapon. It can print money at will, and can simply order its banks to lend; this is a communist-command economy, after all. Lucent is now a $2 stock - but China won’t go down that easily…

…China doesn’t have the kind of social safety net one sees in the developed world, so it needs to keep its economy going at any cost. Millions of people have migrated to its cities, and now they’re hungry and unemployed. People without food or work tend to riot; to keep that from happening, the government is more than willing to artificially stimulate the economy, in the hopes of buying time until the global system restabilizes.

It’s literally forcing banks to lend - which will create a huge pile of horrible loans on top of the ones they’ve originated over the last decade (though of course we can’t see them). Don’t confuse fast growth with sustainable growth. As I’ve discussed in the past, China is suffering from Late Stage Growth Obesity. A not-inconsequential part of the tremendous growth it’s seen over the last 10 years came from lending to the US. Additionally, the quality of late-period growth was, in all likelihood, very poor, and the country now suffers from real overcapacity.

Identifying bubbles is a lot easier that timing their collapse. But as we’ve recently learned, you can defy the laws of financial gravity for only so long. Put simply, mean reversion is a bitch. And the longer inflated prices persist, the harder they fall when financial gravity brings them back to earth.”

While many key indicators may be looking better the fact that the financial system will take a lot of effort and time to straighten out should not be lost sight of. How much ever smoke screen you create at some point the realities will surface with a lot of pain.

Disclosure: No Positions

Copyright © 2008-09 Tradesense

Subscribe to:

Posts (Atom)

{kind=link}