Last two weeks I did not post anything because frankly nothing seemed to have materially changed. Most of what has been said before in this blog is materializing in specific.

Announcements were made, leaders got together, talks were held and views were expressed and the dire consequences of not cooperating were articulated. But nobody seems to have clue as to how these expressions of world interest could actually/practically be implemented.

China appeared to make some moves (as its China's manufacturing contracted) by

announcing major stimulus package which was the only surprise. Other developments were on the expected lines - Obama got elected, some country specific packages were announced and interest rates were cut by many central banks including US, Europe, Japan.

The lowering of interest rate does not address the leverage and credit issues in the banking system. It works against savers interest and adds to imbalance in finding funds through this source. Interest rates in the first place were not the cause for the problems that have arisen. At best these are like vitamins which may help the patient absorb the main medication better. But vitamins normally are required in small quantities and its excess has little advantage. And it is not actually lowering the cost of borrowing for the corporates.

The banks are using the borrowers’ credit default swap spreads to price credit lines. While this may reflect the borrower risk better the volatility can be high for corporates and in turn financial management that much more difficult.

While the medicines were administered the condition of the patient did not appear to improve and in fact was diagnosed for various not so comforting developments/observations (see below – listed point wise).

Let me explain this a little further.

Many of the moves made by various governments & central banks did make the bull bellow in the last two weeks and we heard many experts calling a turnaround. As I have said before calling the bottom is hazardous in any situation and more so in an environment that is currently evolving. Let me use this opportunity to tell you what I have learnt about Grizzlies. They never want the bulls to hide/die. They need to hear their bellow from time to time to know that their prey is alive and therefore they have their fodder available to them on an ongoing basis. So when in a bear market if the grizzly growl dins it means that it is relishing what it has preyed upon (profit taking). It also makes the bulls to venture out thinking that the grizzly has moved. To the bears this is the way to ensure availability of prey consistently (consistent profit opportunity can arise). In this sense any time the grizzly feels that the bulls may hide or be injured so severely that they may not come back, it realizes that its own opportunities to savor in future may be under threat.

So when bears tire knowing that the probability of getting easy prey is going to get more difficult because most bulls are hiding, it steps back and starts to enjoy what it has in its dish. The greater the destruction of bulls - the more difficult it is to make a come back. It also dwindles the profit opportunities of bears. When the bears find that no matter what they do the bulls are not coming out of their hiding is when they start becoming overconfident and complacent and believe that the battle is won. This laziness on the part of the bears starts giving bulls some breathing space to make an attempt to come together. This is why the market bottoms out well be for the bad news stops – the bears are lazy & the bulls are hiding. Bulls wound heal over time and they get some space to regroup.

The problem has always been to estimate how long the bulls may take to regroup. The circumstances of each bear assault are different and the extent of injury to bulls is also difficult to estimate. If it the regular seasonal changes (business cycle) that leads to it then there are reasonable experiences to fall back upon. But if the assault has been aided by say an earthquake/Tsunami/nuke-attack that hit the bull area and thus provided the grizzly an injured bull to maul. The consequences of this type of assault could be very different as not only the injury much more ghastly, structurally the environment has also been altered. Thus we now need the surviving bulls to get well, read and understand the structure of the new environment, understand how it is positioned therein, see how it can create favorable circumstances/structures/ammunitions to launch its own assault and then wait for the right time to launch it first to recover lost territory before gaining new areas. All this while one has to assume that the grizzly has had so much that it has gone to sleep.

While I have previously posted some of the general structural issues which are evolving that would change the landscape in which future investing is done, some of the specifics that I have gathered in the past two weeks are: (quoted verbatim from reports that I have read)

1. The biggest of all possible financial trends: the eventual bankruptcy of the United States government. Or is it the existing bankruptcy of the U.S. government? The United States government is facing an impending fiscal crisis. Former Comptroller General David Walker calls it a “cancer growing from within.”Even before the bailouts, the Office of Management and Budget (OMB) projected that the 2009 federal deficit would be nearly $482 billion. Since then however, the US government has jacked up spending by the trillions. Some experts even suggest the 2009 deficit could be as high as $2 trillion!

2. Richard Fisher is the CEO of the Dallas Federal Reserve Bank and a member of the Federal Open Market Committee (FOMC )in a speech in May of this year, he stated that the total U.S. debt – including Medicare and Social Security – is more than $99 TRILLION! Along the same lines, Laurence Kotlikoff, a Boston University economist, suggests that the “fiscal gap” – which is the difference between the number above and what we could reasonably expect to collect – is $66 trillion. That is the definition of bankruptcy. It is just a matter of time.Note that foreigners who were funding all this profligacy have started leaving the floor looking to invest the surpluses in their own countries – e.g. China.

3. G20 called for an innovative "college" of supervisors to oversee the biggest global banks. The concept is to have a place where regulators from many countries can gather to discuss a bank's operations. Accounting standards will also be put in place to take account for off-balance-sheet vehicles. It also called for better risk management practices at banks. Another problem was the conflict-of-interest discovered in credit rating agencies. The G20 called for global standards to cover these firms. On hedge funds, the G20 said that finance ministers to assess the adequacy hedge fund best practices. This could be the first step for direct regulation of the sector.

4. With dueling press briefings and statements through the weekend, it was clear that

bridging ideological gaps among nations afflicted with different versions of the economic contagion would provide the new president and other world leaders with a daunting challenge.

There is also a more basic philosophical divide across the Atlantic: Europeans in general favor more state control over markets, even to the point of granting regulators cross-border authority, while the United States stresses the primacy of national regulators. President

Nicolas Sarkozy of France, who called on Mr. Bush to organize the meeting, alluded to those differences, saying the negotiations, even on general principles, had been challenging.

5. In a

surprise turnaround, Hank Paulson, US treasury secretary, said that the remaining funds in the government’s $700 billion Troubled Asset Relief Program would be best used to provide capital infusions to distressed companies and tackle consumer debt, rather than buy illiquid mortgage-related assets. The situation would be difficult to hazard as new jokers come into the pack after January20.

6. UBS clients have been receiving calls and letters telling them that their Swiss accounts will soon be liquidated. Those who have concealed funds from the IRS have two basic choices: They can take new and potentially difficult steps to hide the money, heightening their risk of being caught and punished severely, or they can come clean. The backdrop for UBS's action is that the U.S. government has been pressing UBS and the Swiss government to disclose the names of thousands of Americans with undeclared accounts, while the Swiss have vowed to uphold Swiss legal protections for bank clients. However, as a practical matter, whether or not the Swiss formally give up the names, UBS's decision to close the accounts undermines Switzerland's legendary code of bank secrecy. Swiss banking/Swiss type banking is to change drastically and have hot money flows under severe scrutiny.

7. Just when Wall Street’s leveraged loan headache had subsided to a manageable throb, more pain threatens. The amount of buyout debt stuck on bank balance sheets has dwindled. But loans repackaged for hedge funds are ending up back with banks as the schemes unwind. Worse, no one knows the extent of the potential exposure. At the crux of problem are total return swap (TRS) programs. These have been used to give hedge funds the returns and risks of bundles of junky loans without the need to actually hold them or finance their purchase. The trouble is, a TRS deal usually requires the hedge fund to pony up cash when the underlying portfolio’s value declines. If the fund fails to do so, the lender that financed the portfolio can seize it.

8. Manny Roman, the co-chief executive of GLG, Europe’s biggest hedge fund,

warned that thousands of hedge funds are on the brink of failure. He predicted that between 25 and 30pc of the world’s 8,000 hedge funds would disappear “in a Darwinian process’’, either by going bust or deciding that meager returns are not worth their efforts.

9. The market downturn is

ravaging public pension funds across the United States, with many state and local governments seeing more than 20 percent of their retirement pools swept away in the turmoil. Even before the financial crisis, many large pension funds already were considered to be inadequately funded, according to the Government Accountability Office. The losses could force some states and local governments to ask taxpayers to pay more into the funds or to demand more contributions from the police, teachers and other government employees whom the benefits cover.

Poverty, pension fears are

driving Japan's elderly citizens to crime - just on the sideline of what can happen in other countries too.

10. The problem looming in many established blue-chip companies that pay dividends now and may not later. They have heavy pension obligations bearing down on them. These problems should be stated in financial reports. But sometimes they are hidden in plain sight. A bit of dubious padding in pension plan earnings projections can neatly camouflage millions in shortfall i.e. using dubious discount rates.

11. BoE (Bank of England) calculates that banks would have to shed one sixth of their assets just to get back to the 2003 level of bank leverage. That level is probably too high for the next, more cautious financial era. If banks work too fast to strengthen their balance sheets, loans would be called, asset prices would fall further, trade credit would be reduced and the already expected recession would be deeper. The BoE clearly prefers a slower adjustment with more government help, but in any case the “legacy of overextended balance sheets” is a painful one.

12. Intelligence officials are

warning that the deepening global financial crisis could weaken fragile governments in the world's most dangerous areas and undermine the ability of the United States and its allies to respond to a new wave of security threats.

13. The World Bank said it would make an additional $100 billion available to developing countries over the next few years. Robert Zoellick, the bank’s president, said that “virtually no country has escaped” the financial and economic crisis, but that poorer country were particularly vulnerable to a slowdown in the global economy and decline in world trade.

The other developments that appear to be key and need to be tabbed are:

1. In the span of just a few weeks,

orders for both business and consumer tech products have collapsed, and technology companies have begun laying off workers. The plunge is so severe that some executives are comparing it with the dot-com bust in 2000, when hundreds of companies disappeared and Silicon Valley lost nearly a fifth of its jobs.

2. The one prop to the U.S. economy, which has been exports, is about to get kicked out from underneath it as reports came in that export declined 6 percent decline in September.

3. The Circuit City bankruptcy and the lower outlook from J. C. Penney came as the Commerce Department reported that retail sales plummeted 2.8 percent in October, a record, and were down 4.1 percent from October 2007. Automobile sales are 23 percent below last year’s numbers. Spending at gasoline stations dropped sharply, by nearly 13 percent, as falling oil prices pushed down the price of gasoline. Consumers cut back their spending across nearly every sector, like furniture, electronics and clothing. The data portend a bleak Christmas shopping season that will force retailers to make deep discounts.

4. Citigroup, which a decade ago set out to rewrite the rules of American finance, is bracing for still more pain now that a recession is at hand. Loans that the financial giant made to consumers in good times are going bad in growing numbers. For the moment, profits seem as elusive as ever, analysts say. If you look at their loss rate, it is almost inevitable that Citi is going to be asking the government for more money next year.

5. The Federal Reserve gave American Express the go-ahead to turn itself into a bank. The decision gives America’s only remaining big independent credit-card company greater access to government funding.

6. The prospects of a government

rescue for the foundering American automakers dwindled as Democratic Congressional leaders conceded that they would face potentially insurmountable Republican opposition during a lame-duck session next week. If a deal isn’t made and GM goes bankrupt, we’ll be in store for far more severe economic times than we’ve seen in a long, long time. After all, two and a half million people will lose their jobs in the next twelve months alone.

7. A new report showed that nearly one in five U.S. mortgage borrowers owe more to lenders than their homes are worth.

8. JPMorgan Chase & Co, the largest U.S. bank, said it would halt foreclosures for 90 days as it ramps up a program to make it easier for homeowners to modify their mortgages. Bank of America plans to soon start modifying an estimated 400,000 loans held by its newly acquired Countrywide Financial. Citigroup has started a USD 20bn mortgage modification program.

9. In an attempt to help struggling homeowners in America, the agency that oversees Fannie Mae and Freddie Mac outlined a plan to avoid “preventable” foreclosures. Households that have missed three or more mortgage payments may receive assistance through refinanced mortgages with lower interest rates and longer payment periods of up to 40 years.

10. Investors withdrew a record $70.7 billion from U.S. stock mutual funds in October, according to data compiled by TrimTabs Investment Research. Redemptions by individual investors and institutions jumped 26 percent from the previous high of $56 billion in September

11. The next

critical deadline for hedge funds: Nov. 30, the final day of the year that many hedge fund investors can file to redeem their stakes. Unlike mutual funds, which trade daily, hedge fund customers can request their money only on certain dates, typically once a month or quarter.

12. Its (hedge funds)

latest problems come amid mounting expectations that the hedge-fund community will be decimated by the global market meltdown. Banks have been calling in credit lines extended to a number of funds, which has forced them to sell shares to raise cash.

13. Nicolas Sarkozy is pushing the banks to lend more. The French president extracted promises from the country’s largest banks that lending growth next year would be in the 3-to-4% range. He has gone a step further, saying that government representatives will monitor banks’ behavior in every region.

14. Authorities in Italy, the UK and the US have urged banks not to be too harsh on troubled customers – whether small businesses in need of working capital or homeowners hoping for a break on their mortgages. Unless the credit market eases up substantially, the governments’ lists of worthy borrowers in need of protection is set to lengthen. (So much for health of banks if the governments have their way – a path to more troubled assets).

15. Germany became the latest country to fall into recession since the onset of the crisis. The World Bank and the Organization for Economic Cooperation and Development now predict that the developed world overall will contract next year; even in red-hot developing countries such as China and India, growth is projected to slow. Officials in the 15 Eurozone countries announced that the region had officially fallen into recession.

16. Some

$2.1 trillion of European company and bank debt matures in the next three years, raising "substantial refinancing risk", according to Standard & Poor's.

17. Germany's Commerzbank is interested in a state capital injection, according to sources familiar with the situation.

18. Barclays is canvassing a variety of ways of changing its capital-raising plan after institutional shareholders objected to the terms offered to investors from Qatar and Abu Dhabi. One idea is to issue more capital to existing shareholders on the same terms that the Middle Eastern investors have received. Barclays' investors will vote on whether to support the current plan on November 24 unless it is changed before then.

19. Japan's two-largest banks, Mitsubishi UFJ Financial Group and Mizuho Financial Group, cut their earnings outlooks by more than half on Friday, hit by growing bad-loan costs and a plunging local stock market.

20. Of the $13.6 trillion of goods traded worldwide, 90 percent rely on letters of credit or related forms of financing and guarantees such as trade credit insurance, according to the Geneva-based World Trade Organization. . . .

The cost of a letter of credit has tripled for buyers in China and Turkey and doubled for Pakistan, Argentina and Bangladesh.

Keep track of the turmoil timeline

here.

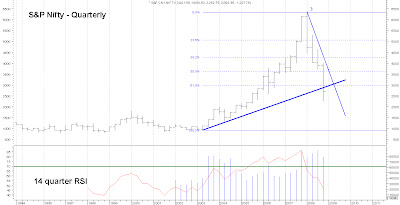

To summarize your care for cash will take care of you!! If you trade be nimble and take your profits ASAP. For longer term investors you will get your opportunity so be patient.

“In terms of valuation, since 1992 emerging market stocks have traded at an average trailing P/E multiple of around 15x. That ratio is now approaching 8x, a record low. For the sake of comparison, the ratio was around 12x during the emerging markets crisis following the Russian default in 1998, and the ratio was around 10x after the collapse of the Internet bubble a couple of years later.”

“In terms of valuation, since 1992 emerging market stocks have traded at an average trailing P/E multiple of around 15x. That ratio is now approaching 8x, a record low. For the sake of comparison, the ratio was around 12x during the emerging markets crisis following the Russian default in 1998, and the ratio was around 10x after the collapse of the Internet bubble a couple of years later.”  “If history is a guide, this re-rating represents an opportunity for long-term investors. Using data since 1992, the table below illustrates the potential for an upswing in the emerging markets when the valuation multiple falls 10 percent below the long-term mean (a trailing multiple of 13.5x or less). Against this background, the current valuation level is even more compelling.”

“If history is a guide, this re-rating represents an opportunity for long-term investors. Using data since 1992, the table below illustrates the potential for an upswing in the emerging markets when the valuation multiple falls 10 percent below the long-term mean (a trailing multiple of 13.5x or less). Against this background, the current valuation level is even more compelling.” “In addition, inflationary pressure will be a critical driver. Inflation has been a vulnerability of many emerging markets in the last two years. There's an inverse relationship between inflation (measured by CPI) and stock valuations, as shown in the chart below. Many economists believe that inflationary expectations have peaked, which if true should be positive for valuations.”

“In addition, inflationary pressure will be a critical driver. Inflation has been a vulnerability of many emerging markets in the last two years. There's an inverse relationship between inflation (measured by CPI) and stock valuations, as shown in the chart below. Many economists believe that inflationary expectations have peaked, which if true should be positive for valuations.”