That the US and the Global economy are moving towards stability has been indicated by the rising oil and base metal prices as well as the stock market performance from the middle of March09. The surprising jobs data at a job loss of 345k against a much higher expected number, while did reaffirm the fact that the US economy is moving back to normalcy, the stock market reaction which one would attribute to such a margin of surprise was missing. Clearly this seems to have some other implications which the players are factoring-in.

Explanations could be along these lines.

-Home prices appear to have hit bottom in some areas of the country, but construction remains weak.

-The auto industry and retailing remain in distress. The job market is likely to remain in the doldrums for many months.

-A home foreclosure crisis is growing … As more foreclosed properties land on markets, real estate prices are falling further, adding to the losses and uncertainties confronting banks.

-Wage growth has been stagnating even as gasoline and medical costs rise, putting pressure on household finances. Average hourly wages were 3.1 percent higher last month than they were in May 2008, but the month-to-month increases in April and May were just 0.1 percent, to a seasonally adjusted $18.54, from $18.52, according to the Labor Department. Wages for manufacturing workers fell 0.1 percent.

-The jobs report presented a statistical puzzle. After shedding an average of more than 700,000 jobs each month during the first quarter, the economy lost 504,000 jobs in April, according to revised data, and the number was smaller still in May. Yet the unemployment rate leapt from an already high 8.9 percent, reinforcing fears it would reach double digits.This disconnect owes to the way in which the government collects data. The number of jobs comes from a survey of employers, while the unemployment data is derived from a survey of households. In April and May, the number of people who told surveyors they were actively looking for work increased by more than one million. These people would have previously been considered outside the work force and thus excluded from the unemployment calculation. Now, they are officially back in the hunt, yet struggling to secure work.”And to me this discomfort comes from the rising treasury yields. Says a

NYT report“The Treasury’s benchmark 10-year note fell 30/32, to 94 7/32, as investors edged away from buying government debt in the face of exploding federal deficits.

The yield, which moves in the opposite direction from the price, rose to 3.83 percent, from 3.71 percent late Thursday, and was up from 3.46 percent a week ago.

The creep toward higher interest rates represents a return to normalcy in some ways…

But higher interest rates on Treasuries make it more expensive for the government to borrow trillions in new debt, and they also raise mortgage rates for home buyers, threatening the government’s efforts to keep borrowing costs low.

But higher interest rates on Treasuries make it more expensive for the government to borrow trillions in new debt, and they also raise mortgage rates for home buyers, threatening the government’s efforts to keep borrowing costs low.”

This is something I have mentioned in my

previous post as a key risk for the US market and is now emerging an important headwind.

A Miller Tabak + Co., LLC report brings out the concerns even more clearly:

“The action in the two year note today where the yield is up a dramatic 30 bps to 1.25%, the highest since mid November, is happening coincident with a move higher in yield in the fed funds futures contracts where the market has somewhat reset their expectations of what the Fed will do. The fed funds futures are pricing in a 48% chance of a 25 bps rate hike by the September 09 meeting and that is up from a 2% chance priced in just yesterday.

After today’s better than expected payroll figure being the main catalyst for today’s action in conjunction with the ever growing inflation concerns, the Fed needs to decipher what is a readjustment of growth expectations and/or what is related to inflation concerns and whether they will fight these trends in order to keep interest rates low.

Reading comments from Fed President and voting member of the FOMC Yellen within the past 15 minutes does not give much confidence that they know what’s going on and it seems that they had very little of a game plan going into their QE policy. Using quotes from DJ, she said that while buying MBS and US treasuries got off to a good start with yields heading lower, “there’s a lot that central bankers don’t know about the magnitude and duration of the effects of these policies” and “our standard monetary policy models do not incorporate financial frictions that lead to asset purchases having real effects.” She went on to say “we lack both the data and theory to provide strong guidance on these policies” and “we are sailing in uncharted waters, marking our maps with every bit of information along the way.” Yellen is a career economist and ex school professor so she’s learning first hand what its like to mess with the market. I’m worried if other Fed members are this uncertain.”

Fed not knowing what it is up to is a concern

expressed before.

Another

commentator albeit in a different context brings home the point regarding the long term yields.

“Listen, what really matters to energy prices these days is the perceived value of the dollar and the perceived ability of the government to stop its massive spending binge. Oil has been moving because of the disturbing widening of the yield curve that seemed to suggest that the government’s ability to keep rates down in the long end would make every dollar the government spends that they do not have more and more expensive to pay back. Oil moved because it saw the threat posed by the widening yield curve and it expressed those concerns with soaring gold and silver prices, ratcheting up copper prices. Not to mention talk in recent weeks that the untarnished best in the universe debt rating of the United States of America’s was even rumored to be downgraded.And you Mr. Grumpy Bernanke have to go ruin it all by saying enough is enough. Why tell the Senate and Obama and the rest of America that we can’t have our cake and eat it too? I like cake! Don’t tell us that we cannot have it all like universal health care, finance Social Security, buy out auto companies, bail out Fannie and Freddie, massive stimulus packages and speculating in the green energy space and at the same time drive down the dollar and make commodity speculators rich. What kind of downer talk is that? Whenever you think that way remember there has never been anything false about hope. We have faced down impossible odds. We've been told that we're not ready, or that we shouldn't try, or that we can't afford it because our budget deficits threaten financial stability or we can’t because of our threatened ability to borrow indefinitely to fund a budget deficit that already this year is estimated to be $1.85 trillion, equivalent to 13 percent of the nation’s GDP the highest level since World War II. Or that we can’t because we are on path that will make this country bankrupt, just remember that generations of Americans have responded with a simple creed that sums up the spirit of a people. Yes we can! Yes we can! Commodity bulls all over the world thank you.”

Assuming the US authorities do get their exit strategy right and is able to balance the rate vs. growth concerns - will the global developments allow this to happen? To me it looks extremely difficult. According to a Natixix special report:

“The rise in long-term interest rates (particularly in the United States) is very bad news, since a fall in long-term interest rates was the only policy left for central banks.

What accounts for this rise?

− Inflationary risk due to the scale of monetary creation? But if expected inflation rises, there is no real inflation risk and, moreover, the US and European economies will remain very weak for a long time to come;

− Crowding-out effects due to the size of the expected public debts? But private indebtedness continues to fall and the savings rates keeps rising;

− Contagion from higher returns that can now be obtained, for instance on emerging-country equities, due to the economic recovery in Asia?

This third argument (correlation of bond yields in the United States and Europe with returns on other financial assets) seems the most reasonable in our view; it corresponds to a return of capital flows to emerging countries.”

And will emerging countries be able provide a much higher sustained returns to keep this flow sustained. To me this looks a possibility although it does tread into the decoupling argument which I had dealt in a

previous post.

Natixix looks at China’s ability to sustain a 9%+ growth on the following lines. In the context of the growth in credit in China (which can be applied to many large emerging economies) it says:

“…However, if there is to be a risk of a credit crisis in the future in China, similar to the one that has unfolded in the United States and Europe, the country would need to lack any other possible engine of growth.

In the United States and Europe, if credit had not outpaced incomes, growth would have been close to potential growth, i.e., in view of productivity gains and growth in the working-age population, around 2.25% in the United States, 1% in the United Kingdom and 1% in the euro zone. Credit was used to ensure more robust growth than would otherwise have been recorded.

On the other hand:

“Productivity gains, in China, are accounted for by what are normal factors in an emerging country:

− Migration from the countryside into cities, as the productivity of migrants improves significantly, as is reflected by the income differential between cities and the countryside;

−Very high level of investment;

− Technology transfers via direct investment.

…growth can be estimated at 9% per year at least. There is accordingly no reason why it would be necessary, in a normal situation, to boost demand by credit in China, and this in fact explains the medium-term stability of the credit-to-GDP ratio in China...

...The causes of productivity gains in China are durable, and this implies that potential growth will remain robust for a long time, resulting in a situation where there is no long-run need for a sharp rise in debt ratios.

In the United States and Europe, the low level of potential growth in comparison with the robust growth one wants to achieve has led to a steep rise in debt ratios being used, and this sparked the crisis because of excess indebtedness.

In China, the current economic recovery is driven by credit; but there are exceptional circumstances with, for instance, the decline in China’s exports due to the contraction in global trade.

In a normal regime, productivity gains are high and potential growth is robust in China, and this rules out the need for a durable increase in indebtedness to stimulate growth.

However, it may well be that the current vigorous upturn in credit, driven by the government’s instructions, with loans extended at very favorable conditions for borrowers, could lead to the reappearance of non-performing loans in banks’ balance sheets, and the Chinese government will likely have to pay for them in the future as it already has done in the past.” (US & Europe are no different)

.Disclosure: No PositionsCopyright © 2008-09 Tradesense

-CDOs, as shown by the tightening in CDS spreads (Charts 2A and B);

-CDOs, as shown by the tightening in CDS spreads (Charts 2A and B);

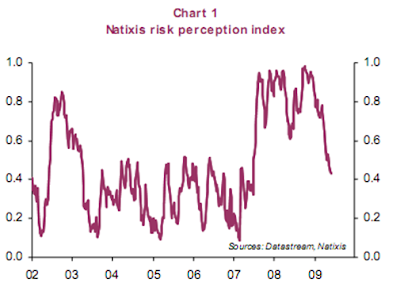

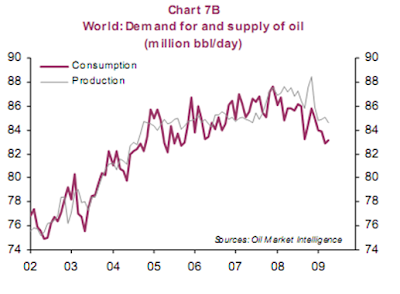

As soon as investor risk aversion decreased, asset price bubbles reappeared: surge in emerging-country equities (Chart 6), rise in the oil price despite the situation of excess supply in the market (Charts 7A and B).

As soon as investor risk aversion decreased, asset price bubbles reappeared: surge in emerging-country equities (Chart 6), rise in the oil price despite the situation of excess supply in the market (Charts 7A and B).

This demonstrates:

This demonstrates:

{kind=link}